Investor Intel: Antimony – Critical or Strategic or Both?

Investor Intel: Antimony – Critical or Strategic or Both?

Written by Christopher Ecclestone for Investor Intel and published on June 21, 2021

China has a very strong position in Antimony and long has had. Indeed this is the metal it has been dominant in for the longest. However, like so many other resources this was squandered through overproduction, predatory pricing and high-grading. China now finds its domestic share of global production plunging and to prop up its dominance it has become a leading importer of artisanal and “conflict” ore from all around the world. It then processes this imported ore/concentrate and manages to hold a still dominant position in processed end-product Antimony Trioxide and other products.

Is the metal strategic? Thus far it does not have the type of sexy applications that other high-tech metals possess, but it is still a key component in the things it is used for such as fire retardants and its historical application as an alloy used to harden Lead in ordnance/ammunition and Lead-acid storage batteries.

And now the latest new technology to utilize the metal is Antimony molten salt batteries for mass storage. The potential here is for a quantum surge in demand. This new application may be its own undoing if the price of the metal goes too high and unravels the economics.

Lighting a Fire Under the Price

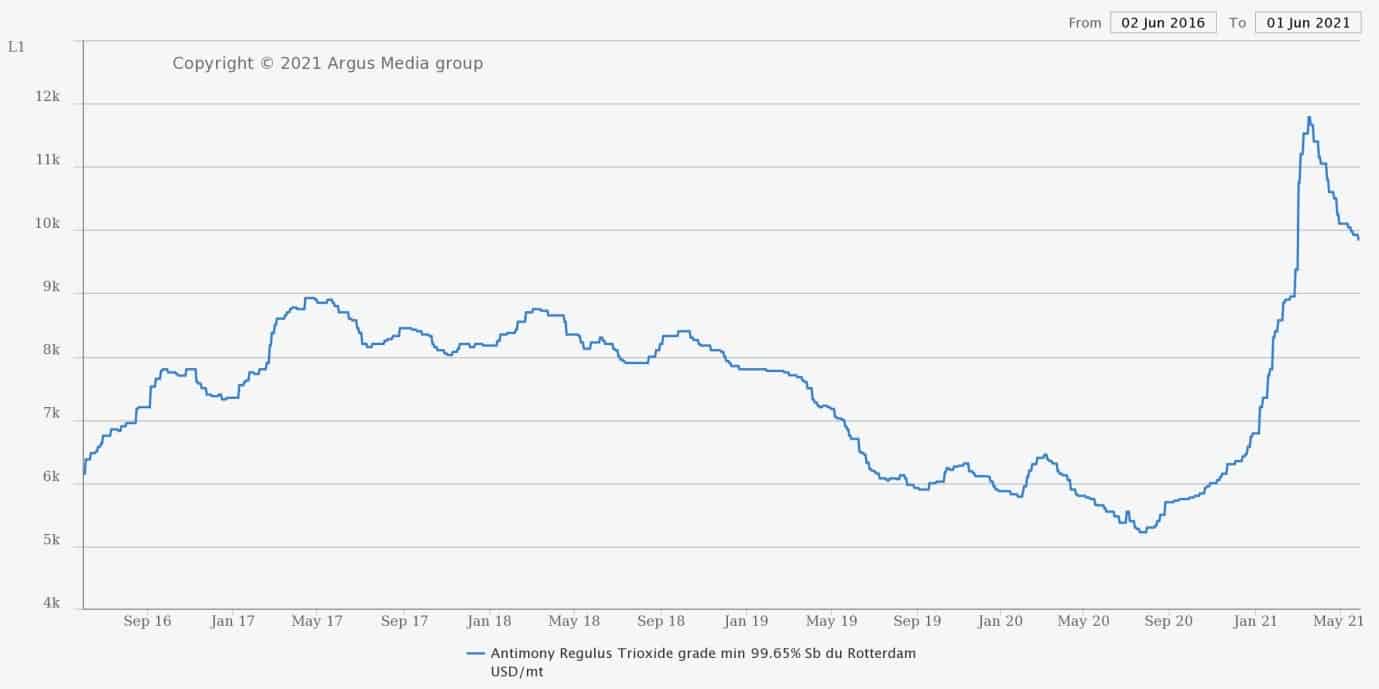

After a price slump that lasted several years, and sank the prospects of several Antimony wannabes, the price of Antimony started to uptick in 2016. It got to around $8,500 per tonne and then plunged again to around $5,500. That price was the result of a regulator-induced swoon over the use of the metal in fire retardants in children’s pajamas (the culprits being the EU and State of Massachusetts), however the main application in fire retardants has not gone away and in the wake of Grenfell Tower fire in London the regulators act against fire retardants at their own peril. This was further complicated by the ever-looming liquidation of the FANYA stockpile, which amounted to around 19,000 tonnes, which was finally sanctioned by Chinese courts in 2019. The talk in the trade was that the FANYA stocks were bought by one of China’s largest Sb producers.

Source: Argus Metals

In the wake of the pandemic and with the marketplace dry of product, the price has had a fire lit under it by Molten Salt batteries capturing the Zeitgeist. This move was compounded by global shortages caused by the Pandemic, the coup in Burma, long term underinvestment, declining Chinese production and the arrival of Molten Salt batteries in the commercial marketplace.

The worries about regulators evaporated like Gorillas in the Mist in the last quarter of 2020 and a stampede to rebuild stocks occurred sending buyers (notably in the US) into a feeding frenzy with Antimony becoming the hottest metal in the last six months (though tussling with Tin for that title) doubling in price from around $5,500 in late 2020 to nearly $11,000, from where it has eased back slightly.

On the supply-side protracted low prices have stymied anything beyond small-scale production by artisanals outside China.

Molten Salt Batteries as Icing on the Cake

We have written before on how Molten Salt batteries, based on Antimony are starting to make waves. If Liquid Metal Batteries become the “killer application” in grid-linked storage (or non-grid linked) then it potentially lights a fire under Antimony demand and pricing. The announcement that United States Antimony Corporation (NYSE: UAMY) had secured an offtake deal with Ambri for its output lit a fire under the price of that stock in late 2020.

To mix some metaphors, molten salt batteries have flown under the radar thus far but definitely have a place in the evolving battery universe and hopefully will take the Antimony market along for the ride.

In this Third Wave of battery metals, Antimony (the prime component in Molten Salt batteries) has joined the ranks of battery metals and the hunt is on for that scarce commodity, the non-Chinese Antimony miner.

Each GWh of Ambri batteries requires around 1% of current annual production of these (calcium and Antimony) anode and cathode materials. This is the closest we have to divining how much Antimony that the Ambri product line might consume if it gains traction. Current Sb production is around 170,000 tonnes per annum, implying that a Gigawatt of Ambri cell utilizes 1.7 tonnes of Antimony.

Thin Pickings amongst Actual & Wannabe Producers

Despite the metal price excitement, the equities markets are starved for options in this metal. The small field consists of the gold/silver miner, Mandalay Resources Corporation (TSX: MND) that has Antimony as a by-product from its Costerfield mine in the Australian state of Victoria, and United States Antimony with its curious focus upon the Los Juarez Silver-Antimony mine in Mexico. Red River Resources Limited (ASX: RVR), another developer basically focused on gold is trying to revive the Hillsgrove mine in New South Wales (which has Sb as a by-product) and Perpetua Resources Corp. (NASDAQ: PPTA) which was formerly called Midas Gold, has a mega project in Idaho (again with a gold focus) that also has the potential to supply half the current US demand for Antimony displacing China as the main supplier to the US. It will be interesting to see if the price surge broadens the offering in equities markets.